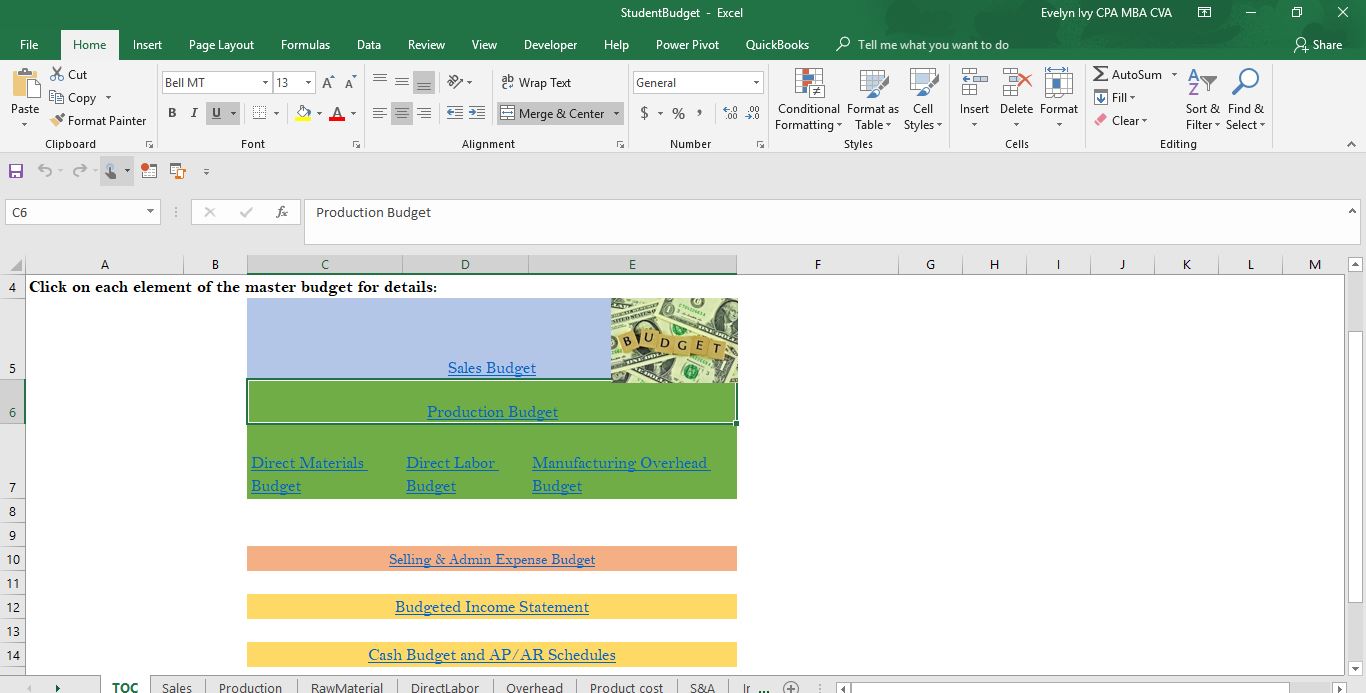

The master budget consists of various sub interrelated budgets. The goal is to deeply think of all areas affecting the business goals and develop a plan of action to meet those goals.

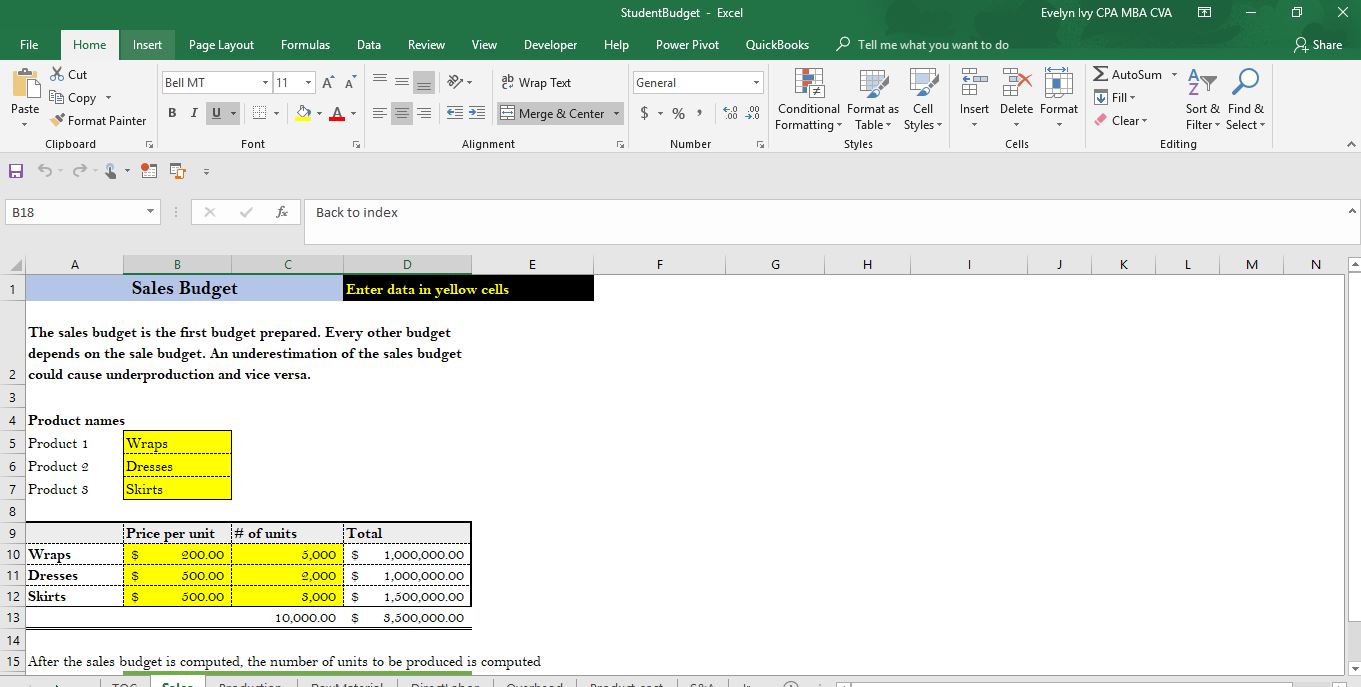

The master budget starts with projecting sales. After sales projections the following sub-budgets are created:

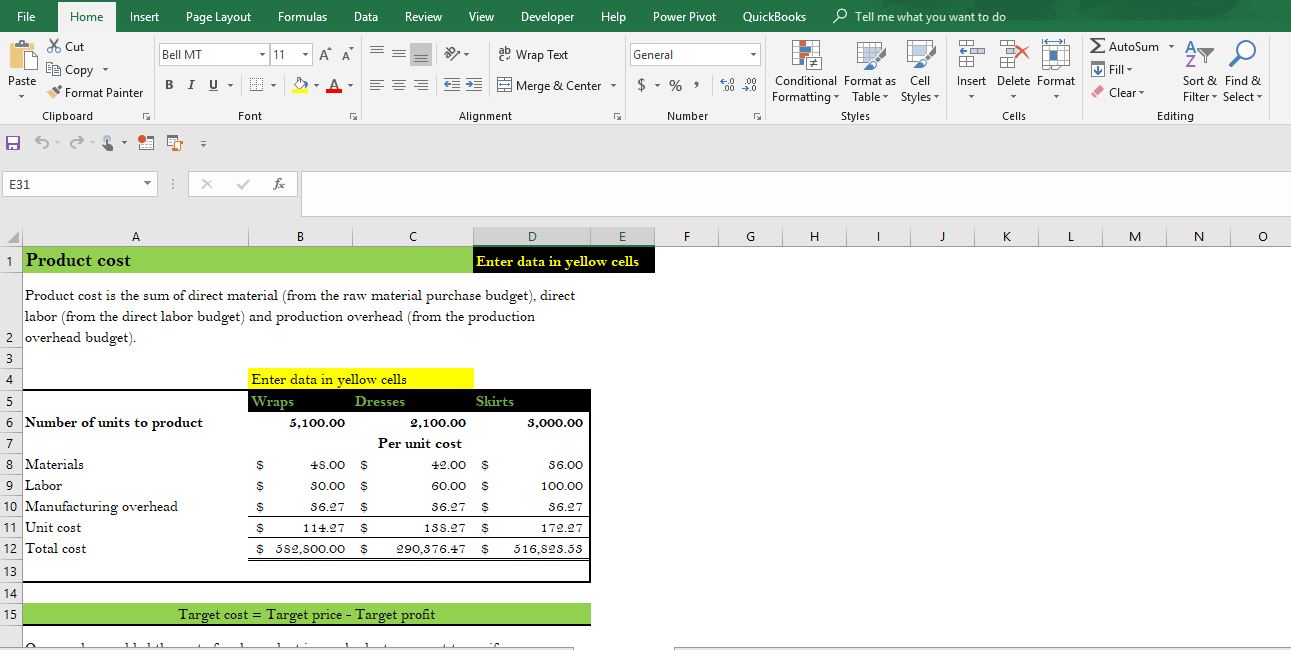

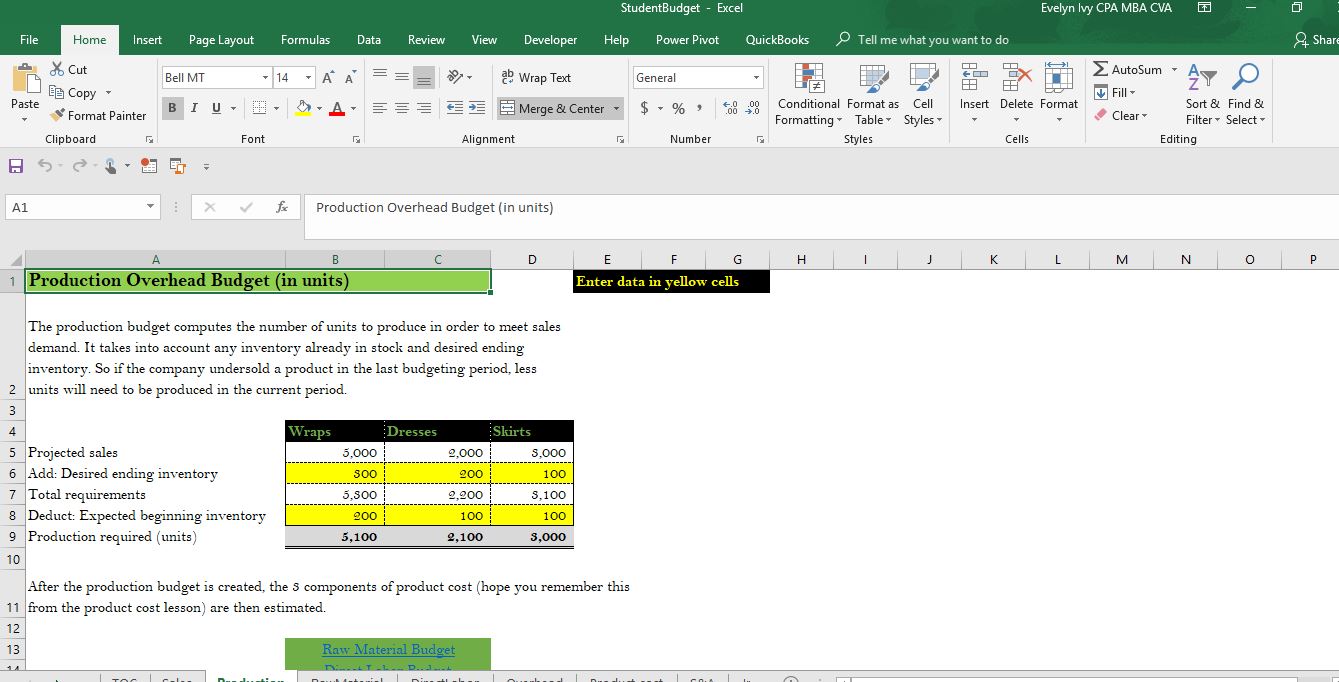

- Production budget: computes how many units should be produced to meet the sales goals

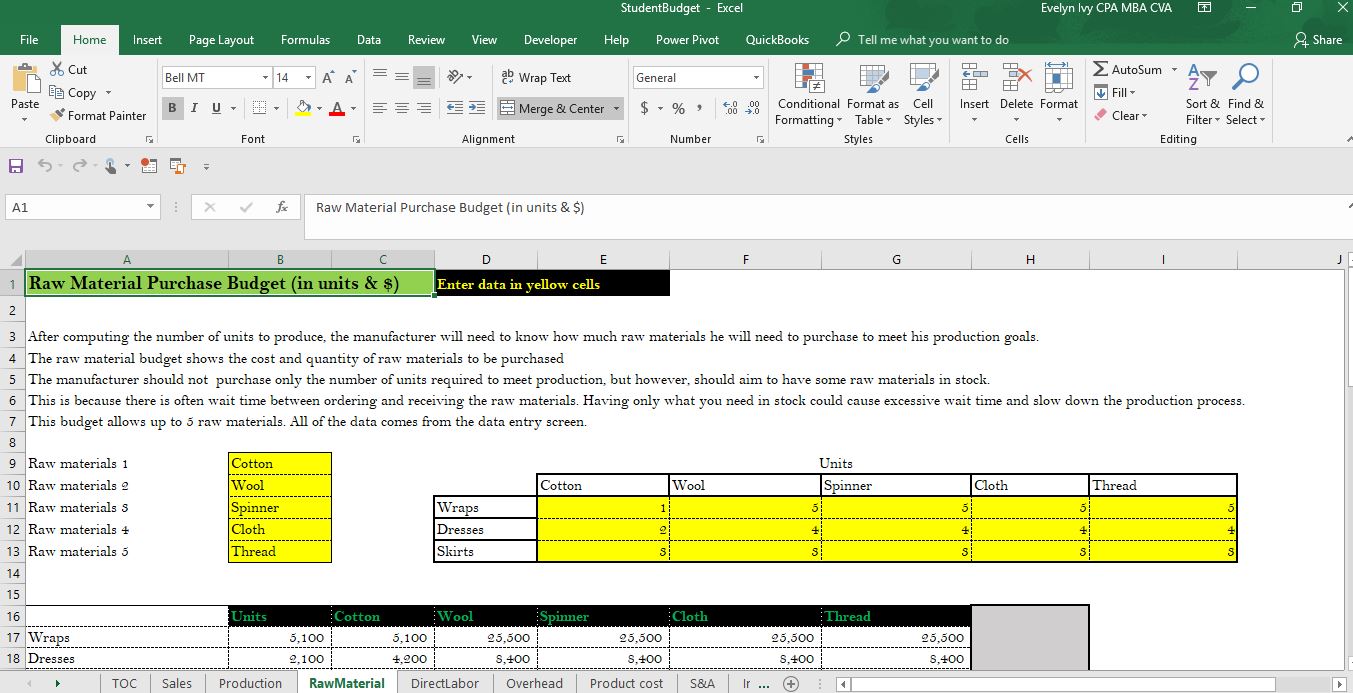

- Raw materials budget: computes how much raw materials should be purchased to produce the number of units calculated in the production budget

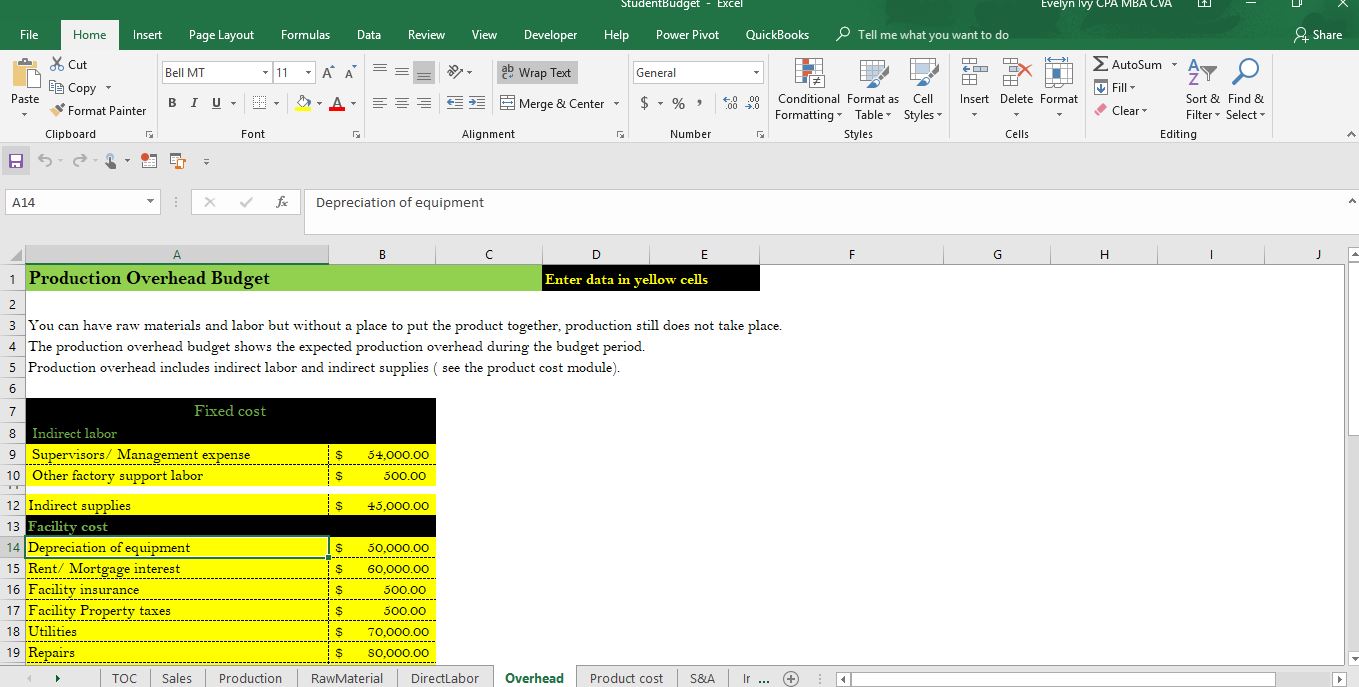

- Direct labor budget: Estimates direct labor cost to meet the production goal

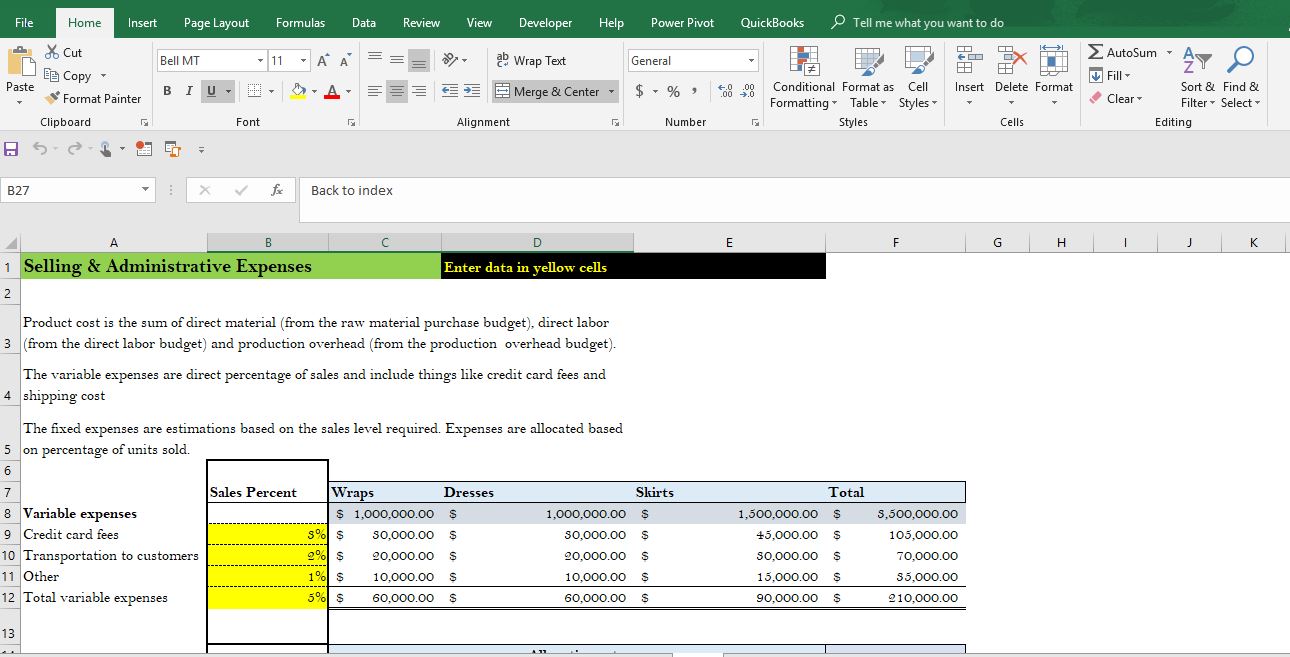

- Selling & Admin budget: estimates the expenses needed to meet the sales goal outside of production.

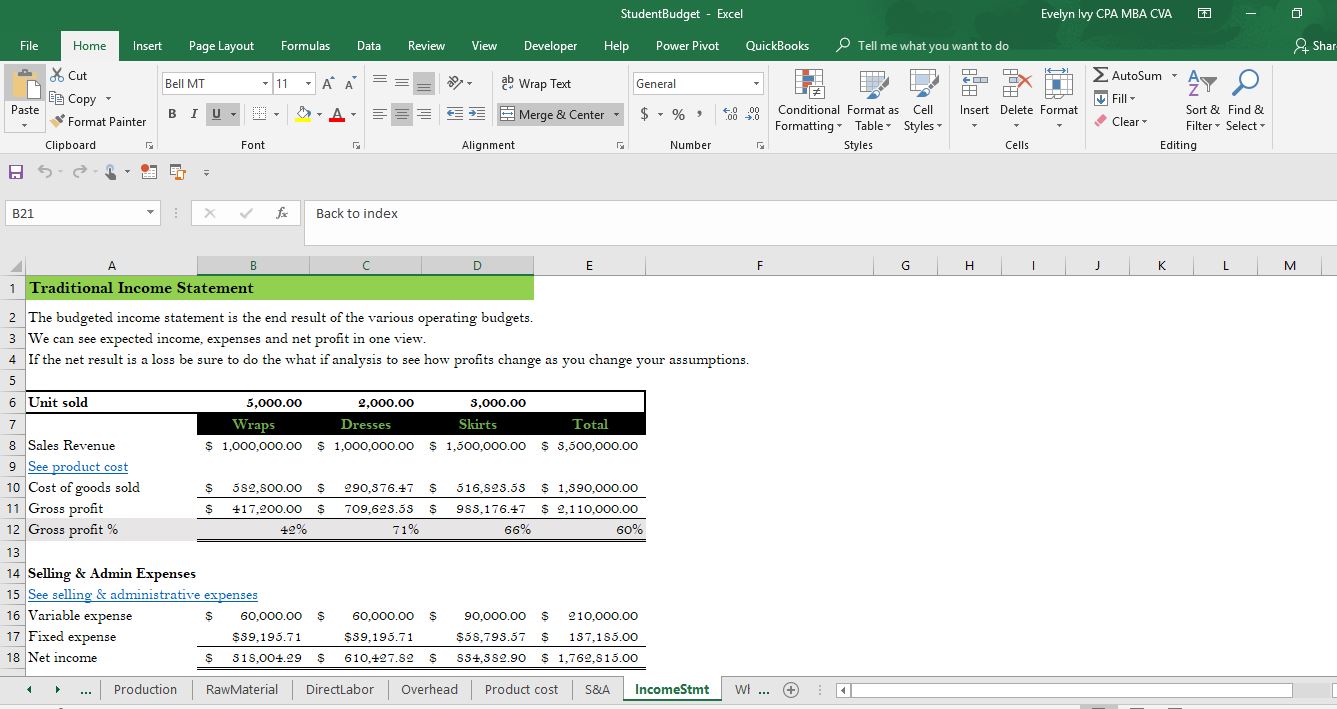

- Income statement: The end product of the budgets described above is the budgeted income statement.

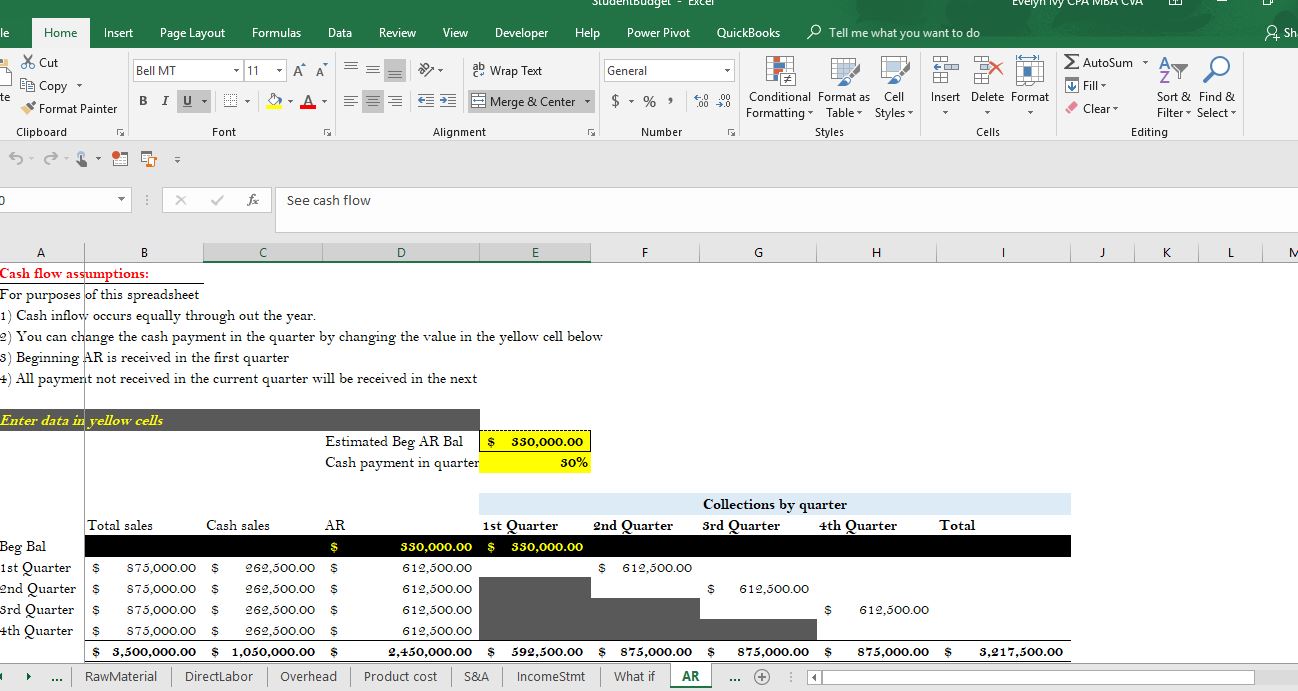

- Cash flow statement: As we know cash flow does not equal profits. This budget estimates expected cash inflow and outflow